GDP GROWTH DATA

The GDP Growth Rate for 2017 Quarter 2 was officially 3.1%, comfortably above the 15-year mean, which includes the 2007-2008 recession. It’s the best quarter since Q1 2015 (3.2%) but not close to the high of Q3 2014 (5.2%). It’s a decent number, but of note is that “private inventory investment increased“, which is fine as long as consumers show up to buy said inventories, but consumer confidence, while still high, has slipped from 96.8 in August to 95.1 in September and is down from 98.5 in January. It has not been below 70, however, since 2011.

GDP Growth Rate – 15-Year (1/1/2002-10/7/2017)

GDP Growth Rate – 4-Year Trend (7/1/2013-10/7/2017)

FEDERAL FUNDS RATE DATA

Two big pieces of news came from the Fed in the last few weeks. The first is that the federal funds rate will remain unchanged, neither increasing (which would signal an expectation of inflation related to rapid growth) nor decreasing (which would signal perceived weaknesses in financial markets). This lack of change however is hard to read in light of the other major news, which was a discontinuance of quantitative easing, and selling back the $4.5 trillion in debt that has been accrued since the 2007-2008 recession. The era of easy money is officially over, and the training wheels that have been helping the US economy have come off.

Federal Funds Rate Rate – 15-Year (1/1/2002-10/7/2017)

Interbank Loan Rate – 15-Year (1/1/2002-10/7/2017)

INFLATION RATE DATA

The inflation rate dipped down from 1.9% but has recovered since, yet remains below the 15-year mean. The rate is still on an upward trend since at least 2015. The market expects the inflation rate to break 2.0% this month, but a lot of factors are involved in this, most prominently the increase in fuel prices caused by disruptions to fuel refineries on the coast from Hurricanes Harvey and Irma. These fuel price spikes promise to cause market wide price spikes for some time.

Inflation Rate – 15-Year (1/1/2002-10/7/2017)

CAPITAL GOODS NEW ORDERS (Non-Defense) DATA

New Orders of capital goods are still above the 15-year mean, and have been on an upward trend since 2016. However, more recently, new orders have been flat in 2017, leveling off well below their rates in 2013-2015 or even late 2007-2008. The economy seems to be comfortable getting onto the highway but isn’t risking going full throttle. Whether that is because of the continue regulatory and financial burden of ObamaCare (likely) or simple uncertainty of the economic situation likely depends on who you ask. Either or, the market is still performing well below its potential.

Capital Goods New Orders – 15-Year (1/1/2002-7/7/2017)

JOB NUMBER DATA

The jobs numbers have been trending downward since 2015, though, at least until the hurricanes in Texas and Florida, had managed to hold fairly steady in 2017. The one-two punch of Harvey and Irma doused two of the largest economic zones in United States, and the August job number dipped into negative territory for the first time since September 2010. Unrelated to the hurricanes, however, job numbers for July were decreased from 189,000 to only 138,000 jobs, a reduction of 27%. While August numbers were revised upward, there was still a net loss 38,000 jobs between July and August, in addition to the 33,000 (preliminary) lost in September. That’s over -70,000 jobs lost from July to September.

Job Numbers – 4-Year (1/1/2013-7/7/2017)

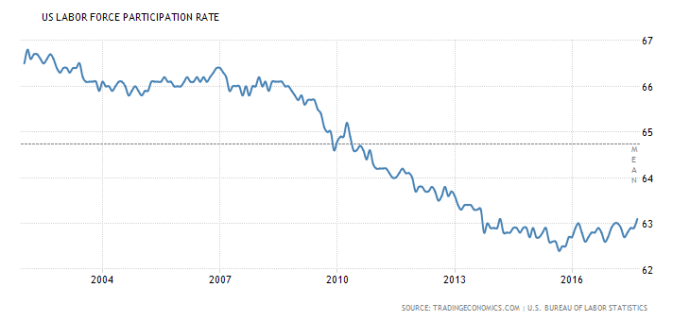

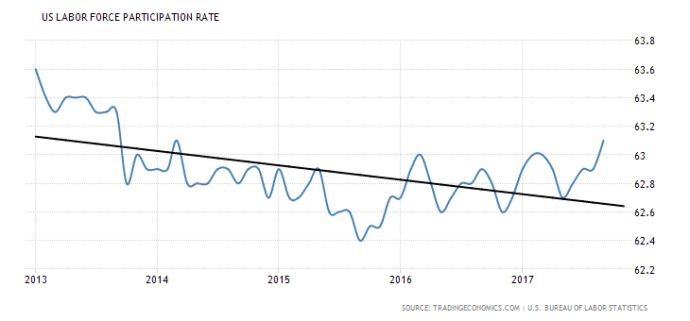

LABOR FORCE PARTICIPATION RATE DATA

The Labor Force Participation Rate (LFPR) peaked at 63.1% for the first time since March 2014, when it hit the same peak. The LFPR remains far below the 15-year mean, with no indication of any increases in the near future. The 4-year trend remains negative with very slow recovery. The promise of large scale increases of manufacturing jobs remains as elusive as ever.

Labor Force Participation Rate – 15-Year (1/1/2002-7/7/2017)

Labor Force Participation Rate – 4-Year (4/1/2013-7/7/2017)

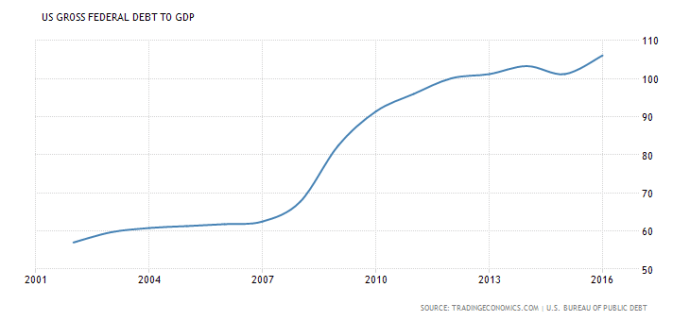

GOVERNMENT DEBT TO GDP DATA

As things are, even if every dollar produced in the United States for an entire year went to paying down the debt, we wouldn’t pay it all. With the debt ceiling looming again, President Trump is reportedly in talks with Democrats about repealing the debt ceiling. That would be like trying to cure cancer by never talking about it, hoping it goes away on its own. The debt ceiling was supposed to protect us from this situation, clearly our politicians do not understand what a ceiling is.

Debt to GDP – 4-Year (4/1/2013-7/7/2017)

THE READ

Despite the positive GDP growth number, other factors, including the employment numbers, with numbers at or around 100,000, continues to be fairly mediocre, even in the best light. The damage caused by the hurricanes and the time lost during recovery will cost billions and cause a mid term hit to job growth, as will the continued increase in long-term fuel prices. The failure to repeal the job killing “Affordable Care Act” remains the noose around the economy that employers hoped would have been an easy win.

The Republican Party has failed to deliver on their promises, with Senate Republicans having failed to come through on any of half a dozen plans to “repeal” ObamaCare, including a clean repeal plan, that they have promised for literally years now. Trump ran on a “repeal and replace” plan that he promised that everyone would love, and that he would quickly and easily negotiate with Congressional Democrats. That still hasn’t come to fruition.

As of now, the economy looks to be stable with a few of the trends either level or increasing in the short to mid term. Four year trends remain downward, however, so these numbers are still digging themselves out of a pull back from recovery highs. With the end of easy money, and the Federal Reserve looking to balance their books, there may be a tightening of capital in the very near future as that $4.5 trillion tab gets cleared. All is not rosy, which is why new orders remain below below the 4-year average.

This has been the Liberty Is For The Win Economic Quarterly. Catch you all in a few months for Quarter 4!

Liberty is For The Win!