Note: In previous quarterly (and monthly) articles, the time frame depicted in graphs was January 1st, 2002 to the date the article was written. This was due entirely to the fact that 2002 was 15 years before the original article, and, for consistency, that date was used for subsequent articles. Graphs will take data from January 1st, 2001 to the present date in order to allow comparison of the Bush, Obama, and Trump economies.

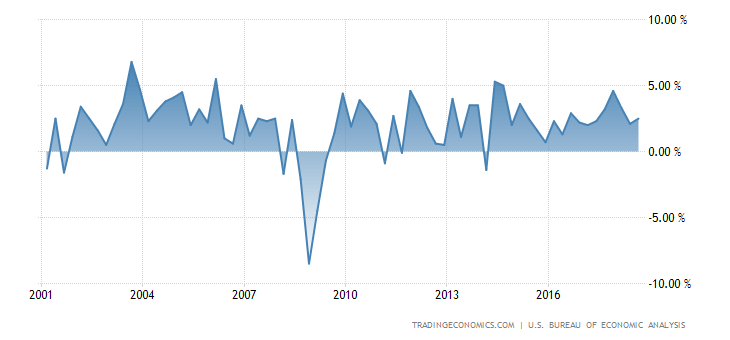

GDP GROWTH DATA

According to the preliminary estimate for the third quarter of 2018, the economy grew at a healthy 3.5% GDP growth rate, exceeding earlier forecasts but tapering off some from the 4.2% of the previous quarter. The second and third quarter results for 2018 are the best back to back performance since the second and third quarters of 2014, at 5.1% and 4.9% respectively. For perspective, the highest quarterly GDP growth rate since 2001 was 7.0% in 2003.

GDP Growth Rate (1/1/2001-10/26/2018)

INFLATION RATE DATA

The inflation rate spent the third quarter steadily falling from 2.9% in July to 2.3% in September. This falling inflation rate has positive implications for wage earners but could be the result of cooling demand. A slowdown in manufacturing around the world indicates that this may be the case and would naturally result in less upward pressure on prices.

Inflation Rate (1/1/2002-10/26/2018)

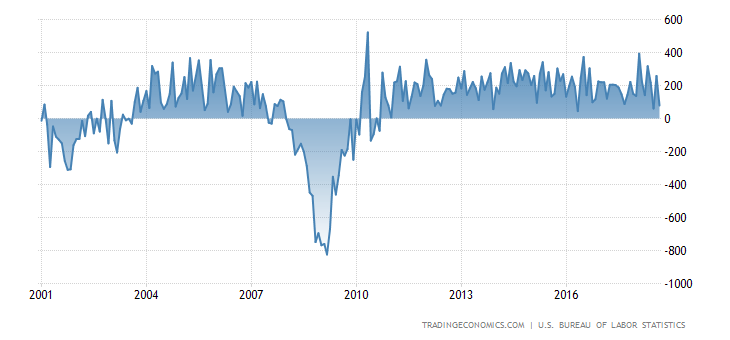

JOB NUMBER DATA

The third quarter jobs number peaked at 270,000 jobs in August but dropped to modest 134,000 net jobs in September. Overall, 569,000 jobs were created during the third quarter, down over 12.5% from the 651,000 jobs created in the second quarter and down over 13% from the 655,000 net jobs created in the first.

Job Numbers (1/1/2001-10/26/2018)

LABOR FORCE PARTICIPATION RATE DATA

The labor force participation rate dropped from 62.9% in July to 62.7% in August and September, putting the US labor force at the same place it was on February 1978. The labor force participation rate has been stuck at about 62.8% (give or take a couple of tenths of a point) since 2014, when it bottomed out, and has shown no signs of improvement in over three years.

Labor Force Participation Rate (1/1/2001-10/26/2018)

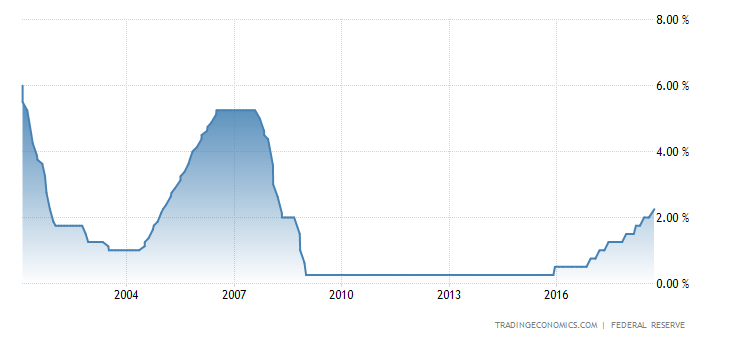

FEDERAL FUNDS RATE DATA

Over the course of the third quarter, the Federal Reserve Board increased the federal funds rate from a top rate of 2.0% to a top rate of 2.25%. While the inflation rate remains at or near their target of 2.0% and the labor market is behaving as though it’s at full employment, the current federal funds rate is well below the long term average of 5.0% and is just now on par with where it was on quarter one of 2008.

Federal Funds Rate Rate (1/1/2001-10/26/2018)

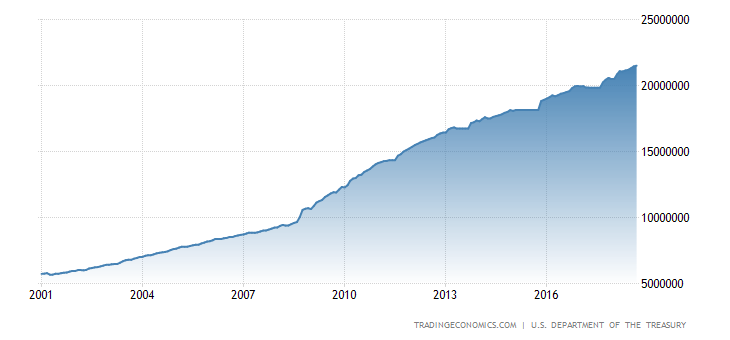

GOVERNMENT DEBT DATA

The federal debt continues to climb from $21.3 trillion in July to top $21.5 trillion in September. The debt-to-GDP for the United States has been above 100% since 2012. Even after several changes in control of both the White House and Congress, very little has been done to slow down the deficits.

Federal Debt (1/1/2001-10/26/2018)

THE READ

There are a lot of things that look good in the last few quarters, and growth remains solid, particularly if the 3.5% preliminary GDP growth rate holds through revisions, but there are still some nagging doubts that won’t go away. Foremost of these is what happens when the training wheels come off of the economy. The Fed has been steadily increasing interest rates over their last few meetings, but we’re still well below the long term average of 5.0%.

While the economy is behaving as though it’s at full employment levels, with wages increasing as demand for high skill workers increase, labor force participation remains at objectively low levels, well below those seen before the 2007-2009 recession. Both the last and current administrations promised to put people back to work, but the stubbornly low labor force participation proves that this simply isn’t happening, at least for low skill workers.

And government debt is still the sword of Damocles hanging over the economic well being of the nation. The sheer number of first tier nations running debt loads at or near 100% of their GDPs remains an ever present threat to the stability of the American economy. As new a new debt crisis in the Eurozone threatens the stability of European trade partners, which includes the United States.

Yes, the economy marked another healthy expansion in the third quarter, but we have to remember that much of the growth was driven by gains in investment and banking. As the stock market corrections of October may indicate, that pony ride is probably coming to an end, and, with the top federal funds rate at 2.25%, the monetary policy is already firmly on the accelerator.

Liberty is For The Win!